3 June 2016

Will the CMA report make any difference to the problems with our banks?

It’s taken me a few weeks to get through the 405 pages of the Competition & Market Authority’s proposed fixes to the UK banking market.

I’m still not sure that any of it is going to make an awful lot of difference. But you can’t accuse them of not trying. Two years, millions of pounds and hundreds of pages of reports later and we’re finally nearing the end.

The main recommendation – as previously flagged in its interim report - is still the introduction of a banking data feed. The main thing this will facilitate is a comparison of different bank accounts based on each individual’s usage.

And that is certainly to be applauded. Too many people choose their accounts based on the wrong information, and are confused by the many moving parts that make up every bank account.

Helping consumers make better decisions is an important part of the challenge of fixing the competition issues in the banking sector. But there’s another much greater challenge which won’t be fixed by the remedies in this report.

Overcoming the fear factor

Most people can’t be bothered to switch. No matter how bad they are treated, no matter how much is being offered in incentives to move – they just don’t want the hassle. They don’t want the risk of one of their direct debits not being paid. They don’t want to be left without a working bank card for a second. So unless the transition can be seamless and devoid of any hassle, most people won’t do it.

The CMA took a good hard look at this problem –and decided that the best way to tackle it is to simply add a few bells and whistles to the Current Account Switching Scheme. They will extend the amount of time that banks have to offer a guarantee when people switch. And while this may provide some reassurance to a minority of customers, the authors of the report admit that it’s unlikely to increase switching of itself.

It’s a great shame that the CMA have dismissed the idea of introducing portable account numbers – which to my mind are an essential ingredient if we’re to increase the number of switchers.

If you could keep the same account details, no matter who your bank was, there would not only be zero risk of your direct debits going astray, but you could even continue using your existing bank cards until your new ones arrived. The switch could truly be seamless. If people knew they could pick up a £100 switching incentive by simply filling in a 5 min application form, they would surely consider it. As things stand, it’s a much more involved process.

As great a shame as it is, that appears to be a battle that is lost for now.

Quantifying good service

The part of the CMA paper that was most interesting to us at Fairer Finance were the proposals to force banks to publish data about how much their customers like them, and how they perform on a number of different service metrics.

The CMA’s idea is to get an independent polling company to survey a decent sample of each bank’s customers, and then force banks to publish the results on their websites – including details of how they compare to their peers.

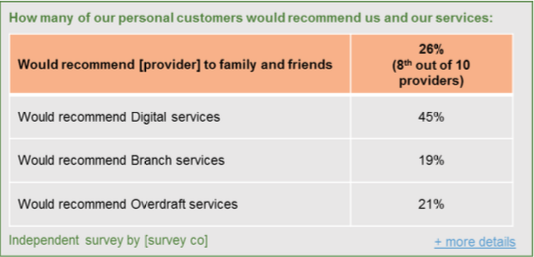

So a scorecard may look something like this:

While I like the idea, I have some concerns about the focus on customer polling data.

When I set up Fairer Finance, I felt it was important to create a scorecard for banks that combined customer views with some other more objective measures. That’s why our ratings combine customer polling results with complaints stats and our own transparency analysis as well.

Can you trust customer polling?

The problem with customer polling data is that it turns up uneven results. Retail brands, for example, tend to do better because of transferred loyalty from the high street stores. M&S Bank, for example, gets an undeniable high street halo.

Banks with more affluent customers who don’t tend to go past their overdraft limits are also more easily pleased. First Direct undeniably offers great service. But it also excludes people on lower incomes – which saves it from some of the difficult conflicts over overdraft charges that its competitors have to face.

I do like the idea of giving customers more information, however.

And showing people how much they could save by switching to another bank – and explaining where their existing bank ranks on their circumstances – would be incredibly potent. From what I understand, however, the current report is merely proposing that banks tell new and existing customers about their comparative service levels – something which I doubt will have much impact.

One thing I’m keen to advise against is the use of star ratings, or anything similar, when displaying customer polling data. I think it should be up to regulators to mandate the publication of data, and up to third party providers to manipulate it in such a way that makes sense for consumers.

Sunshine remedies

The other part of the CMA’s sunshine proposals is to force banks to publish a number of other service metrics. These are set to be determined by the FCA – but could be things such as how long each bank takes to handle a complaint. Or how long it takes to answer the phone.

These data sets will be invaluable to organisations like ours. Customer perceptions can be unreliable. But properly audited, standardised service metrics will give us a much clearer idea of how banks are performing.

So I’m hopeful that the CMA proposals will improve the way that customers choose their banks. That’s important for first time customers, and the small number of switchers.

Increasing switching, however, is a bigger challenge that looks to be left in the too hard to solve box. If we’ve ruled out portable account numbers then perhaps we could look at rolling contracts for bank accounts – rather than simply allowing banks to sign people up indefinitely. That generates plenty of switching in the mobile phone market – and would provide a proper trigger for people to reconsider who they bank with.

About the author