11 December 2014

A mis-selling or a mis-buying scandal in the annuity market?

The conclusion of the Financial Conduct Authority's review of the annuity market confirms what most observers in the world of personal finance have known for well over a decade: insurers have been taking advantage of consumers' lack of knowledge about their retirement options for years, and the consequences for many have been severe.

Buying an annuity is unlike any other financial transaction. You've got one shot to make the right choice, and if you get it wrong, you're left paying for your mistake for the rest of your life. In the worst case scenarios, people have locked themselves into deals that have left them tens of thousands of pounds worse off.

As much as I'd like insurers to have to compensate those who they took advantage of, I'm not convinced that what's taken place in the annuity market over the past decade could be called a mis-selling scandal. I've no doubt that there are many individual cases of mis-selling - but this was not on the kind of scale that, say, endowments and PPI were mis-sold. In the case of annuities, it's been more of a mis-buying scandal - with insurers entirely complicit in steering their customers towards poor outcomes, but largely managing to stick to the letter of the law, if not the spirit of it.

Regulatory failure

To my mind this is more of a regulatory failure - part of the FSA's miserable legacy. I remember writing for the Sunday Telegraph about the poor deal that many people were getting on their annuities well over a decade ago. In the intervening period, hundreds of thousands more people have slept walked into a poor retirement deal. This is not an issue that regulators have been unaware of - it's simply been an issue that they've not been brave enough to tackle until now.

Each of the incremental changes that have been made over the last 10 years have been as ineffective as the last. In many cases, wake-up packs - which were created to try and alert retirees to their options - were simply used as an opportunity to try and bamboozle customers with too much information. This invariably drove them to plump for the easiest option (and often the worst one for them financially).

The Government's older persons' tsar, Ros Altmann, has written a powerful blog today, claiming that she believes the FCA still hasn't grasped the problem. She's called for immediate action to stop mis-selling and bolder steps to clean up this market. As a consumer advocate, it's hard to disagree with anything Ros says, but I'm willing to give the FCA a little more credit. Where they've found evidence of mis-selling, I'm sure they will act on it - and if companies are continuing to ignore the messages coming out of the regulator, then they can expect to be on the end of even heavier fines.

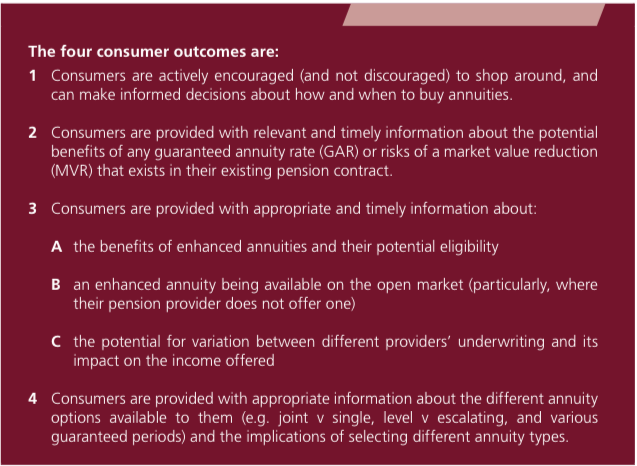

As for future retirees, the FCA has made some good suggestions that will be unpopular with insurers. For a start, annuity companies will be forced to show their customers how much they could get by shopping around - and to ensure that smokers or people with medical conditions understand that they could do better with an enhanced annuity. These are the outcomes that the FCA is striving for, and they seem spot on:

What I took away from the FCA's paper today is that going forward there will be a greater emphasis on companies to prove that they are guiding customers towards the right outcomes - rather than simply taking advantage of their ignorance.

A clearer message

There's certainly more for the FCA to do - as it acknowledges. The industry can't be left entirely to their own devices to come up with clearer advice - they've had their chance to do that and failed.

But I also don't think we should assume that consumers are incapable of making their own decisions in a complex market - they just need a bit of additional protection, so that the worst case scenario for those who are apathetic or disengaged is not financially catastrophic. There may be a thing or two we can learn from auto-enrolment and the National Employment Savings Trust (Nest) here, where people are defaulted into a sensible long-term pensions investment strategy, and can't accidentally lock themselves into something that doesn't fit their appetite for risk.

As the FCA acknowledges, the new free pensions guidance service, which begins in April, will play a key role in ensuring that more people make the right decision in retirement. And the message to insurers is becoming ever clearer: if you are knowingly pushing your customers towards the wrong decision at retirement, you are on the wrong side of the regulator.

About the author