23 February 2022

Are ‘insurtech’ startups making pet insurance fairer?

Insurtech startups, which made headlines in 2021 by attracting record investments, are starting to pose a real threat to established insurance giants. They are up-and-coming in the US and in continental Europe (especially Sweden, arguably the ‘home’ of the pet insurance industry, with Swedish insurer Agria founded in the 19th century). The UK market has also seen several of them appear in recent years, from Bought by Many (founded in 2012 and hailed as a success story) to recent entrants Only Paws and Frank (both incorporated in late 2021).

Instead of offering low premiums and using economies of scale to make a profit, like traditional insurers, these firms attract customers by offering tech solutions and extras that aim to lower claims rates, encourage disease prevention, and make dealing with insurance easier. Waggel, for example, offers an all-digital claims process, ‘hand-picked’ member rewards and policy tracking in their mobile app. Many brands offer a 24-hour vet or nurse video chat service, so owners of poorly pets can get instant access to expert advice. In a trend started by the Swedish insurtech company Lassie, greater emphasis is placed on educating owners about preventing injury and illness, thereby lowering claims rates. In a slightly different approach, Petsure focuses on insuring elderly pets or those with pre-existing conditions – tapping a higher-risk market that traditional insurers did not dare to touch. Insurtech firms might hope that by being more literate about the data they collect, they can find profitable ways to insure such ‘high-risk’ customers.

Besides turning a profit in original ways, these new players also often claim to be fairer to or better for customers. ‘Pet insurance sucks. So we changed it’, claims Waggel on their home page. Frank describes itself as ‘[h]onest, simple, game-changing pet insurance’, arranged by people who are ‘also majorly pet obsessed, which means we always put your furry friends first.’ Napo promises that ‘[w]e don’t want to make money by wriggling out of claims. Instead, we want to prevent vet bills in the first place by giving you free access to some of the best pet care services’. As Fair Value Assessments approach, in the wake of the FCA’s new Consumer Duty regulations, it is important to assess whether insurtech is actually doing better, as it claims.

At Fairer Finance, we rate pet insurance brands based on Customer Experience (CX) and on how their products measure up to our ‘red lines’, an array of criteria which we set to evaluate fair value. To be rated for CX, a brand has to reach a certain threshold of respondents in our nationwide polling, which is conducted every six months. Many insurtech brands are small or are just starting out, and so are yet to appear in these ratings. However, Bought by Many, one of the fastest-growing challenger brands, has maintained a confident first place in our customer experience ratings since Autumn 2020, and has earned a gold ribbon in every round of assessment since Spring 2020. It seems that features like quick, online claims processing and apps that make interaction easier for policyholders are setting these firms up to do well in terms of customer satisfaction and trust. It would not be surprising to see more Insurtech providers score well for customer experience as their customer base grows and more of them meet our polling threshold.

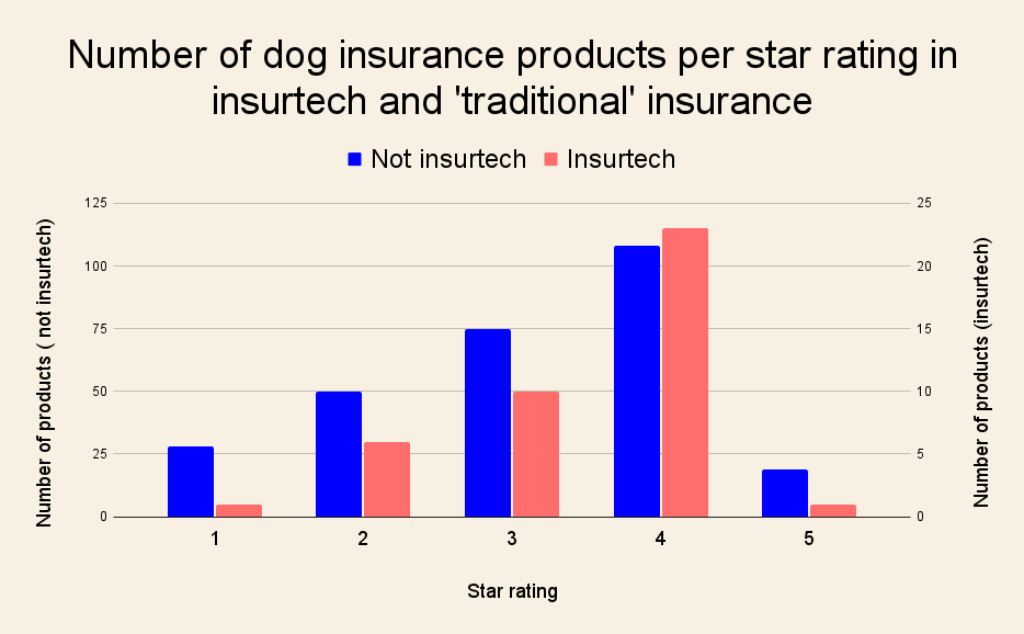

Product ratings is where the picture becomes more mixed. They show that while on average, insurtech brands do better than their competitors, fewer of their products get 5-star ratings.

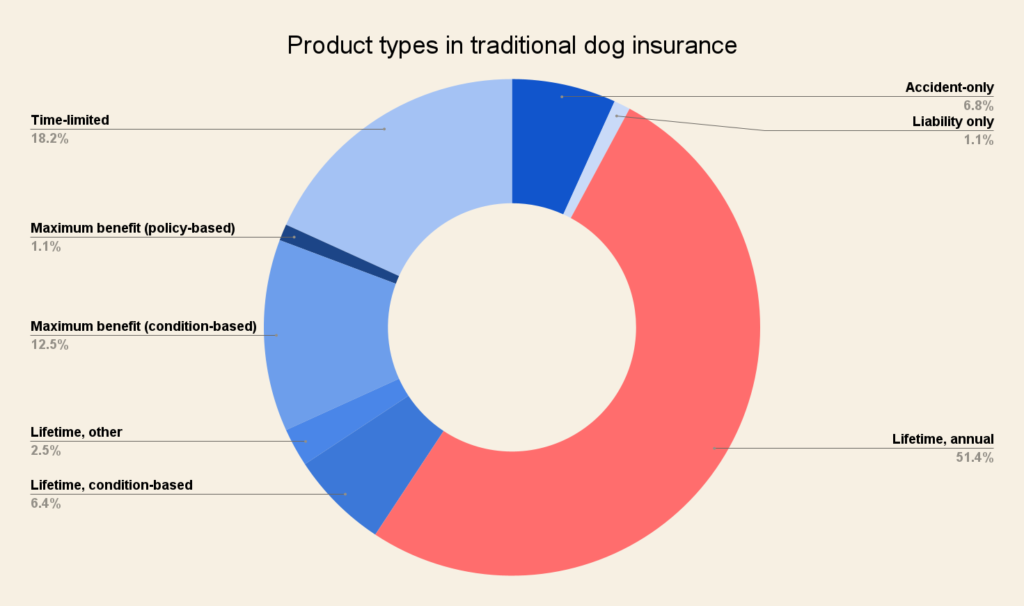

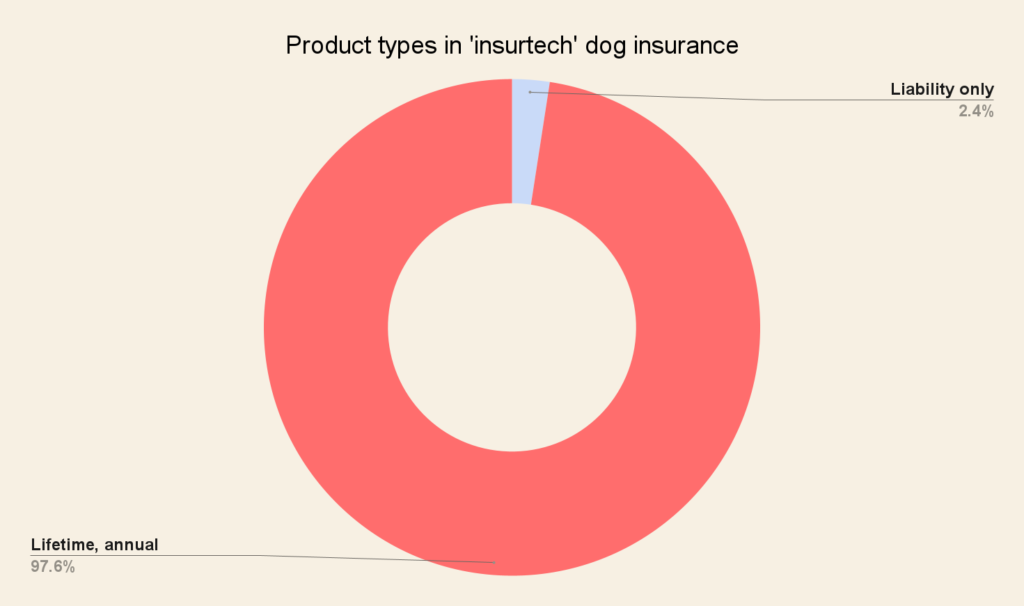

There are two key factors that explain this distribution. First, it is a welcome feature of most insurtech brands that they overwhelmingly offer lifetime policies. These are policies that cover medical costs up to a limit that is reinstated each year, and that usually provide cover for ongoing conditions. Many traditional brands keep lifetime policies as their premium range and offer time-limited or condition-based coverage by default, which generally score worse on our ratings.

However, insurtech products mostly fail to score five stars because they tend to rely heavily on add-ons. Often called ‘boosters’, these are extra product features that are available for a higher premium. While add-ons are often presented as making insurance more ‘customised’, they also mean that the base products are less comprehensive than in traditional insurance.

Insurtech firms are up-and-coming and are already a force to be reckoned with. Traditional insurers can – and increasingly do – learn from the customer experience benefits of the more customer-facing approach and better technical proficiency offered by insurtech providers. However, to keep up their momentum, the new disruptors should aim to improve the quality of their coverage. Focusing on prevention and ease of use is all well and good, but what most customers who purchase insurance will ultimately want is excellent coverage when trouble strikes.

Fairer Finance's Insight Portal gives you a unique understanding of your customers and products. Drop us an email at corporate@fairerfinance.com to start your 14-day free trial

About the author