10 December 2014

The FCA’s £3.8m error

When the FSA was washed away and replaced with the FCA last year, many people suspected that the change would be nothing more than cosmetic. A change of font, a bit of desk swapping, and business as usual.

This couldn't have been further from the reality. The FCA has been much braver and bolder than its predecessor - regulating on the front foot rather than waiting for each crisis to happen, and simply taking responsibility for the clean up.

Error of judgement

Back in March, however, it made its first mis-step. Ahead of launching a review into the closed book pensions sector, it decided to brief the media. The result was a front page story in the Telegraph announcing revealing that the review could end up seeing more than 30,000 policies reviewed, and exit fees being banned.

When markets opened the following morning, the share prices of several insurance companies tumbled. And it was several hours before the FCA finally issued a statement to calm things down.

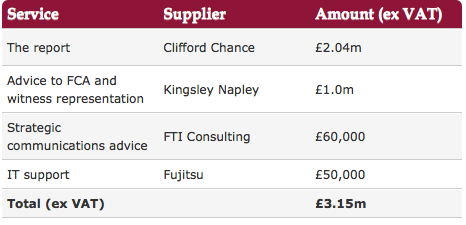

While there's no question that the FCA made a number of mistakes, the response that followed was over the top. Instead of carrying out an internal investigation and taking some clear learnings from the experience, the FCA called in the litigation partner of one of London's largest law firms to carry out a full inquiry. This alone cost a little shy of £2.5m including VAT. The FCA then spent over £1m more on legal advice for its own staff and on communications consultants.

The result was a total expenditure of almost £4m on the independent inquiry.

No conspiracy

It's true that the FCA needs to command the respect of those that it regulates - and needs to lead by example in the way that it conducts its business. But what shines through in Clifford Chance's very expensive report - which was published today - is that the incident in March was an error of judgement. There was no bad intention, no corruption, no conspiracy. Yes, lessons need to be learned, procedures need to be tightened - but spending £4m on an independent report was a colossal waste of money.

It's worth pointing out that this episode has been something of a gift to the life companies - who know very well that the kind of inquiry which the Telegraph story talked about remains a possibility. There are still thousands of people getting a bad deal in closed-book life funds. If £4m had been spent on an investigation into that sector, perhaps we might have seen some much needed action here.

About the author