15 September 2017

The IPID cometh

The financial services industry loves an acronym. From Tessas to Isas, Mifid to Prips, TCF to PCP, the list is endless. And growing.

The latest one that pops up in a growing number of my meetings is IPID.

And If you work in insurance and don't yet know what it means, you definitely need to finish this blog post.

IPID is the Insurance Product Information Document - a new summary that all insurers will be mandated to issue before they sell one of their products - FROM FEBRUARY NEXT YEAR [this has now been delayed - see footnote].

Unlike summary or key facts documents - the forerunners to this latest development - the IPID will have to be delivered in a prescribed template, from which no deviation will be allowed.

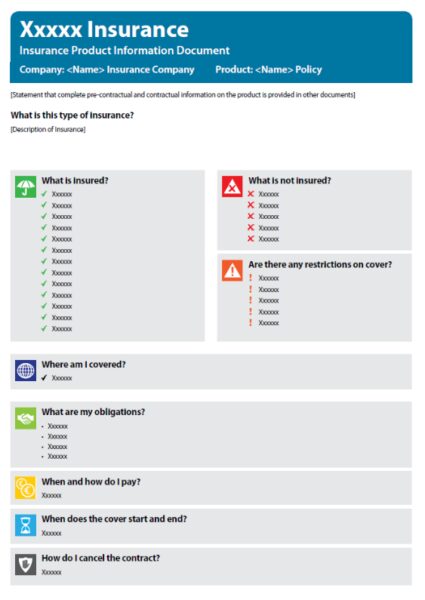

The not very attractive image above is the current draft of what these documents will need to look like. And they'll need to answer the following eight questions:

- What is insured?

- What is not insured?

- Are there any restrictions on cover?

- Where am I covered?

- What are my obligations?

- When and how do I pay?

- When does the cover start and end?

- How do I cancel the contract?

As someone who's spent the last few years trying to persuade companies to innovate in how they communicate with customers, I'm not thrilled about the IPID.

It forces insurers to all use the same question set which itself is not as clear or simple as it could be. Worse still, my experience of standardised templates is that they kill efforts to do better. Everyone feels its acceptable to lower their standards to the level set by the regulators.

Nevertheless, given that the IPID is not voluntary, companies need to get to work developing these documents - and there's still an opportunity here to use this as a chance to improve on what insurers have now.

Given than we are now just six months away from these documents being mandatory, I'd expect there to be a flurry of activity in the insurance industry. I know from first hand experience how long it can make to get new documents written and signed off by the internal workings of a large organisation. But IPIDs do not yet appear to be on most insurers' radars.

If you're about to start work on your IPIDs - here are some tips:

1. Don't let the language used in the questions set the tone for the rest of your document. If the question is "Are there any restrictions on cover?", why not start your answer by explaining the question.

2. Go beyond. Although you have to include the answers to eight prescribed questions in your IPID, there's no reason you can't go beyond this. If there are complexities to your product that aren't easily captured in those eight questions, why not add some more FAQs on a second page. Insurance products are complicated, and I'm not convinced that they can always be easily summarised in a page. If you need more space, use it.

3. Design creatively. There may be some restrictions around how you have to present the IPID form itself, but there's nothing to stop you presenting it with your own branding around. And if you need to spread it out over a couple of pages, then do that. The point of these documents is to help set the expectations of your prospective customers, so don't shrink it down to 6pt font and put it on a sheet of A5. Make sure it's legible.

Like me, you may not be a big fan of the IPID - but it's coming. Use the challenge as an opportunity.

Update: The implementation of the IDD has now been delayed until 1st October 2018.

About the author