The FCA is using the price and value outcome to drive real change under the Consumer Duty. Firms are facing tougher questions than ever before, and – in practice – the absence of evidence may be taken as evidence of non-compliance.

It is no longer sufficient just to have a good fair value framework. Providers must have the analysis of consumer outcomes to back it up. Providers are required to benchmark their products and outcomes to the rest of the market, and analyse the distribution of outcomes that they deliver.

We are familiar with the FCA’s way of thinking, and are close to the latest developments as the FCA begins to enforce the Consumer Duty across the range of financial services sectors. We don’t just repeat what the FCA has said publicly – we provide genuine insight into the regulator’s perspective, and how to meet the regulator’s expectations.

The FCA is familiar with Fairer Finance’s approach to fair value. Our voice is respected and credible in the regulatory community. We always hold up a high bar on the evidence required to demonstrate fair outcomes – passing our fair value tests provide real reassurance. We have deep knowledge of industry best practice, having advised numerous banks, building societies, insurers, and lenders on embedding the Consumer Duty.

Independent review of your fair value framework

The boards and executive teams of banks, insurers, and lenders have asked us to provide assurance over the robustness of their fair value frameworks and analysis. Our external review highlights gaps and provides reassurance over whether the fair value analysis is robust in identifying unfair outcomes and regulatory risks.

We start by reviewing your fair value framework and analysis as applied to a particular product, assessing whether it covers all the bases and asks the right questions. For example:

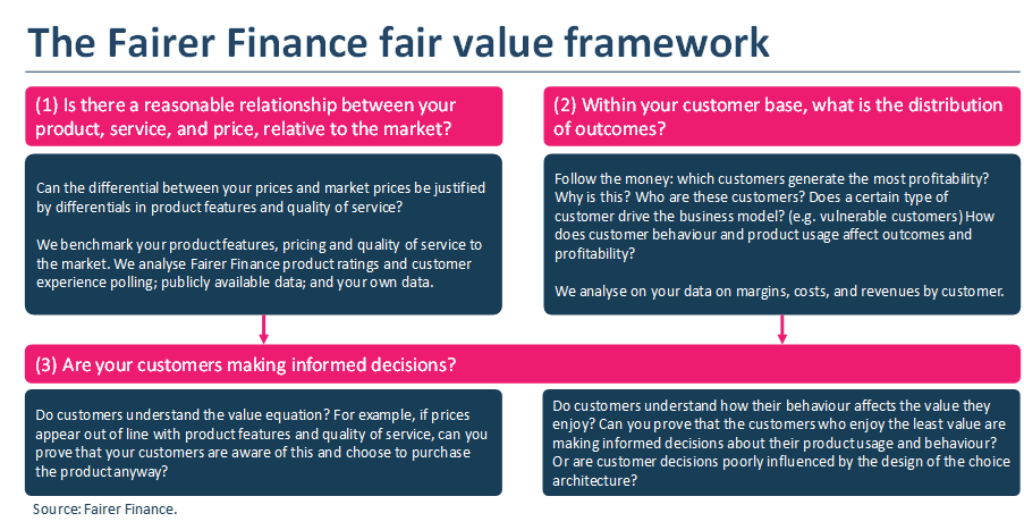

- Does your fair value framework place sufficient emphasis on benchmarking quality, transparency, and service (i.e. not just price) to the rest of the market?

- Does your fair value framework emphasise the analysis of the distribution of outcomes, or does it focus on the outcome enjoyed by the ‘average’ customer?

- Does your fair value analysis get to the heart of the business model? Does it articulate what drives profitability?

Using our fair value framework to evidence fair value

Our tried-and-tested framework assesses whether firms are providing fair value and aims to help them prove it – not just to the regulator but also to customers and other external stakeholders.

We believe fair value is about more than just price. Our framework focuses on ensuring that firms are producing products of suitable quality, and that they are doing everything they can to help customers select a product which meets their needs.

Our existing data sources about the quality of your products and the nature of your customers’ experiences mean that we hit the ground running. We start with a reasonable picture of where your fair value risks lie.

The combination of existing datasets with our skills in behavioural science and data science means our fair value assessments provide a deep level of scrutiny and therefore reassurance.

Consumer Duty horizon scanning

Providers have asked us to ‘kick the tyres’ on their consumer outcomes going forward, identifying the risks that may lead to unfair outcomes. Our independent analysis gives an external view on what might cause the fair value equation to break, and therefore what can be done to mitigate this.

Developing a robust evidence base

The Consumer Duty is about developing the evidence that your consumers are enjoying good consumer outcomes. Providers seek our support in delivering:

- benchmarking against FCA expectations and industry best practice;

- a clear view of risks

- detailed and actionable recommendations on mitigating actions

Ultimately, our outputs are used to underpin best in class product reviews and the annual attestation from boards.

Fairer Finance was instrumental in our work to embed the new consumer duty regulations. Providing a thorough and comprehensive assessment of our current position and actions to take. We would have no hesitation in recommending Fairer Finance, James and the team made an instant impact, taking the time to understand our business. Fairer Finance were great to work with, bringing invaluable insight to our ongoing work.

ARRAN GRAY, COO, SAGIC