23 February 2022

Fair Value and fees for ready-made investment accounts

The FCA’s Consumer Duty paper marks a major change in the way UK financial services firms are to be regulated. In a nutshell, the Duty puts an obligation on firms not just to deliver good outcomes, but also to prove they are doing so.

While parts of the financial services market are hurriedly trying to get their heads around what this may mean for their business, others have already been given a flavour of things to come. Last year, the insurance industry was mandated to do annual assessments proving they are offering fair value, while since September 2019, fund management firms have been forced to produce assessments of value.

In July last year, the Financial Conduct Authority (FCA) published a report on how fund managers had been doing with their new assessments. It’s fair to say the industry got mixed reviews, with the report stating that many fund managers had not done a good enough job. Essentially, too many fund managers made assumptions that they could not justify, undermining the credibility of their assessments. The report stated,

When considering a fund’s performance, many firms did not consider what the fund should deliver given its investment policy, investment strategy and fees. Firms spent a disproportionate amount of time looking for savings in administration service charges that cost investors relatively little compared with the time spent reviewing the costs of asset management and distribution that typically cost investors much more.

While not all fund managers have met the regulator’s expectations, it certainly does appear that the regulations are having the desired effect of bringing down charges.

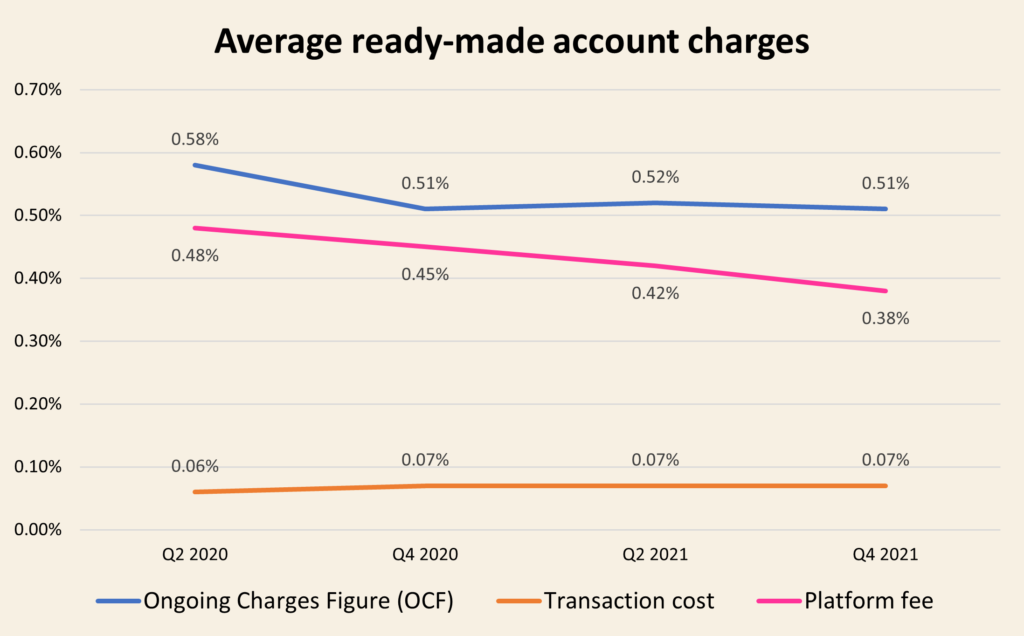

At Fairer Finance, we track the fees that investment platforms charge customers, as well as the fund management fees charged for ready-made portfolios. Since 2020, there has been a steady decline in the costs of investing using ready-made accounts. While transaction fees have remained largely unchanged, platform fees have fallen on average by 0.10 percentage points between Q2 2020 and Q4 2021. Over the same period, the average ‘ongoing charges figure’ (the cost of fund management) fell from 0.58% to 0.51%.

Although fees are decreasing on average, there are still several firms with high OCFs. Bestinvest’s Tilney Sustainable Adventurous Portfolio Clean, for example, charges a hefty 1.55%. While Premier Miton’s High Income Portfolio comes in at 1.69%.

Once the new Consumer Duty comes into force next year, the pressure on firms to lower high charges will increase even more. And as more and more funds cut their fees, it will be harder for those at the margins to maintain their position.

What does a good assessment of value look like, and where is the line for fair value when it comes to setting charges? There’s no right answer. However, you can expect more of what we saw last summer, with the regulator calling out those who are getting it wrong. If you’re not asking the difficult questions and coming up with convincing narratives to justify your charges, you’re likely to end up in the FCA’s next list of shame.

If you would like to talk to us about improving transparency and how to meet the Consumer Duty challenge, please get in touch at corporare@fairerfinance.com

About the author