3 August 2023

The FCA's latest Financial Lives survey reveals some troubling facts about communications in the insurance sector

On 26 July, the Financial Conduct Authority (FCA) published its 2022 Financial Lives survey. This survey has been running since 2017, with the most recent wave concluding in May 2022. The point of the survey - which contains data from 19,145 respondents - is to track public attitudes to financial services.

Some of the most interesting data in the survey relates to what the public thinks about communications from insurers. This data is especially timely in light of the FCA's new Consumer Duty, which emphasises the importance of 'consumer understanding' as a key outcome.

According to the FCA, firms need to demonstrate that their communications 'support and enable consumers to make informed decisions about financial products and services. We want consumers to be given the information they need, at the right time, and presented in a way they can understand.'

What does the Financial Lives survey data suggest about how insurers are doing in meeting this goal?

First, it is clear that more can be done to inform insurance customers about the strengths and weaknesses of the products that they are buying. Only 25% strongly disagree/slightly disagree with the statement that "there is not enough information for me to make decisions about the quality of different policies". This falls to 16% among those with low financial capability (those with low confidence in managing money).

Given the complexity of many insurance products, this is not surprising. Still, there is more that insurers can do, especially on their online customer journeys, to clarify what is and isn't covered by their policies. Examples of good practice are having tables that clearly show different cover levels and exclusions, or highlighting important product information through colour, larger text, or boxes. It is also worth considering whether 'positive friction' can be added to slow down the online journey and make sure the customer understands the key product features.

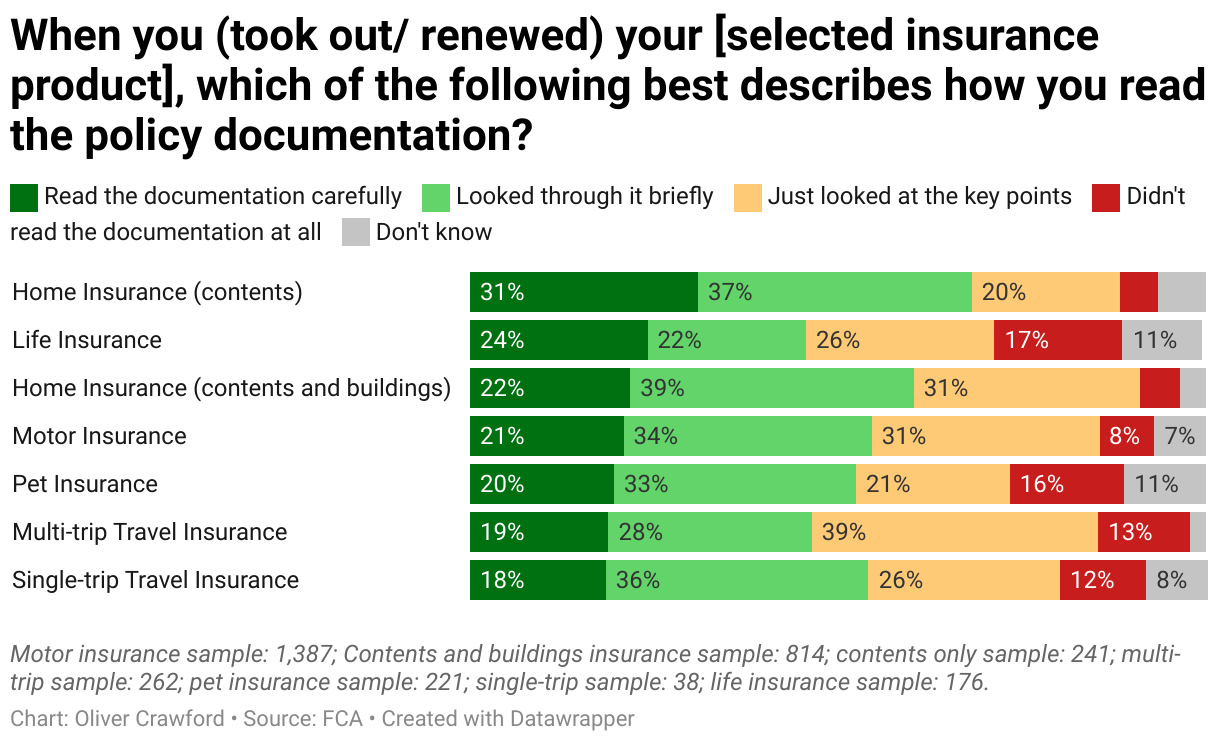

Highlighting key product information when customers are buying insurance is especially important because there is no guarantee that customers will read the policy documentation when they are shopping for insurance or after they've bought it. According to FCA data, only 22% of customers read the documents carefully, on average, while 11% don't read them at all.

This doesn't mean that it isn't important to have clearly written and well laid out policy documents - customers will read those when they have a problem or need to make a claim - but it does mean that providers can't rely on their customers understanding aspects of the product that are only explained in the policy wording. These need to be flagged during the online journey.

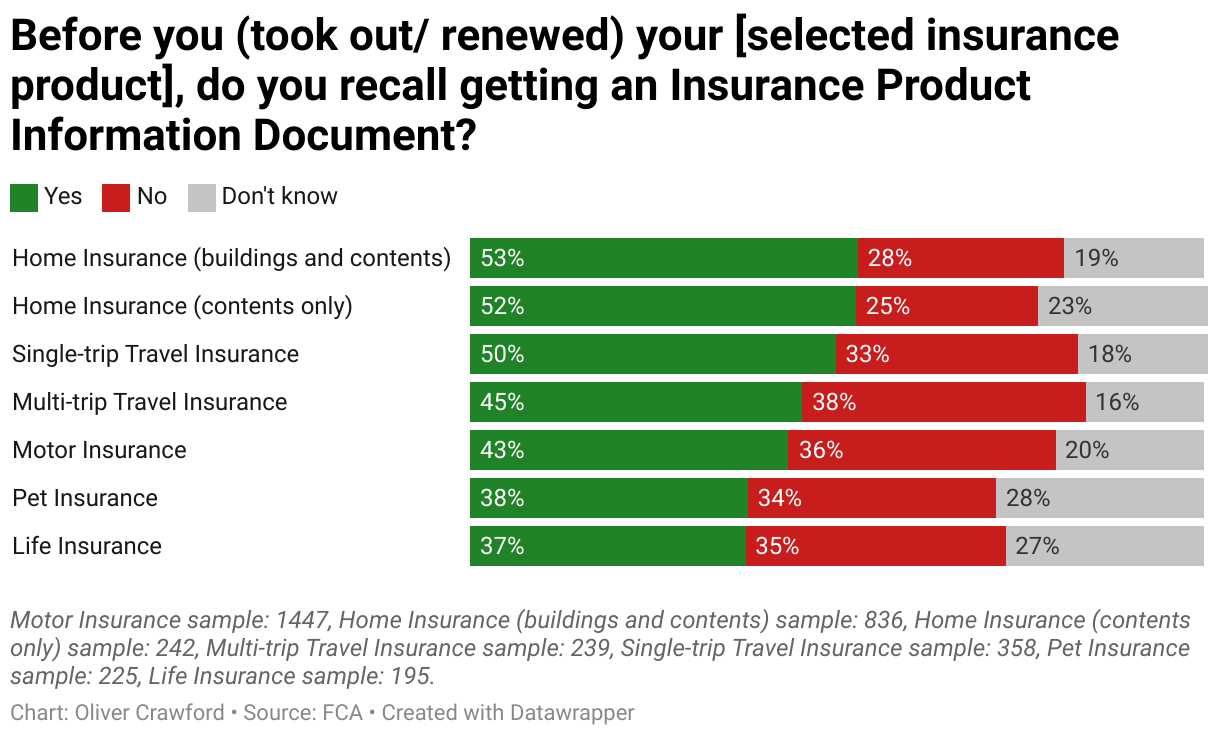

Similarly, providers cannot count on customers understanding an insurance product by reading the Insurance Product Information Document (IPID). Besides the fact that IPIDs are very densely packed with information, which tends to overwhelm customers rather than inform them, around a third of respondents in the Financial Lives survey didn't recall getting an IPID.

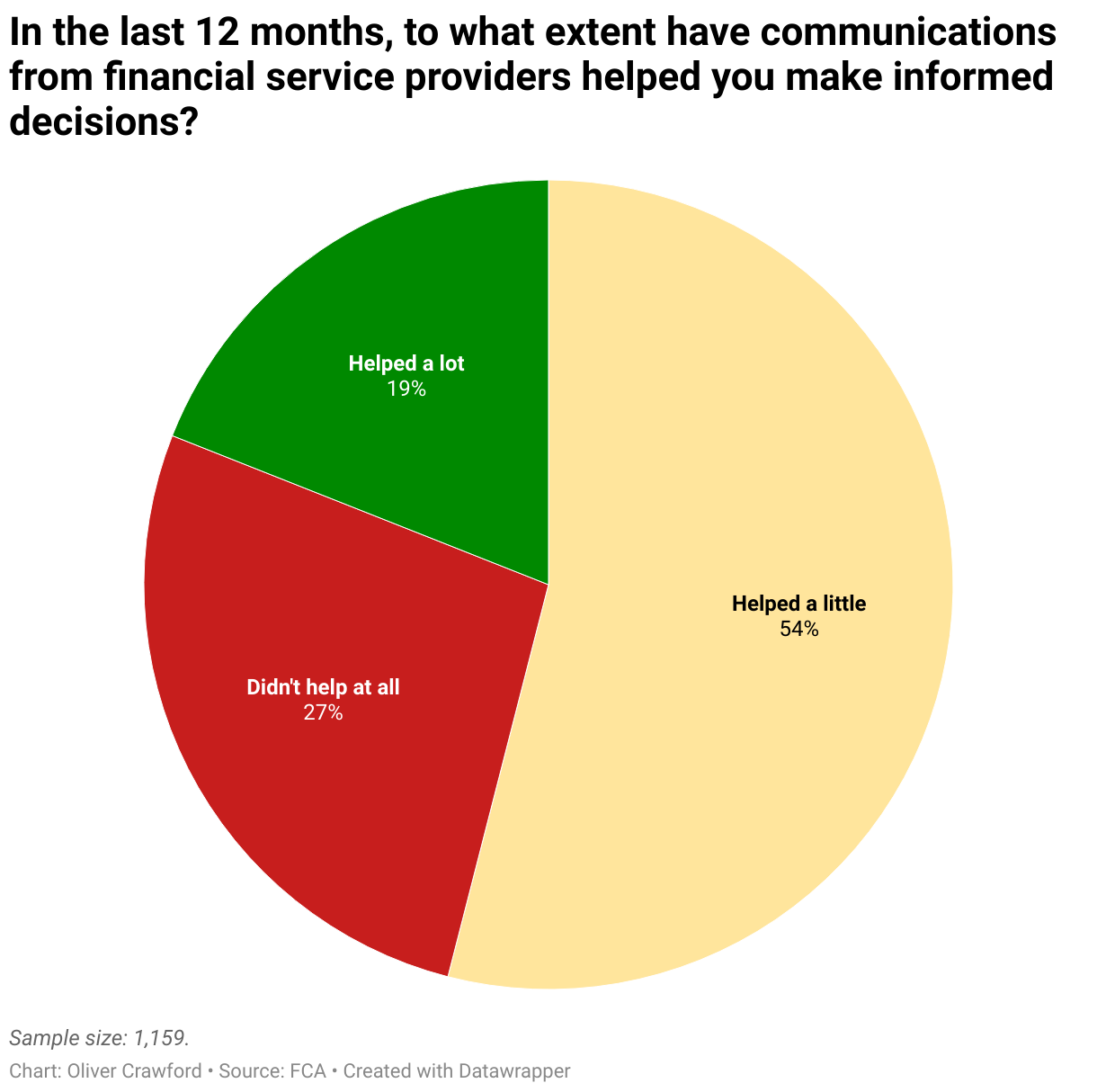

Looking at communications more broadly (which likely includes letters and emails as well as formal documents like policy wordings), the public seem to be mildly positive about how useful these are. A majority say that such communications helped them 'a little' to make informed decisions.

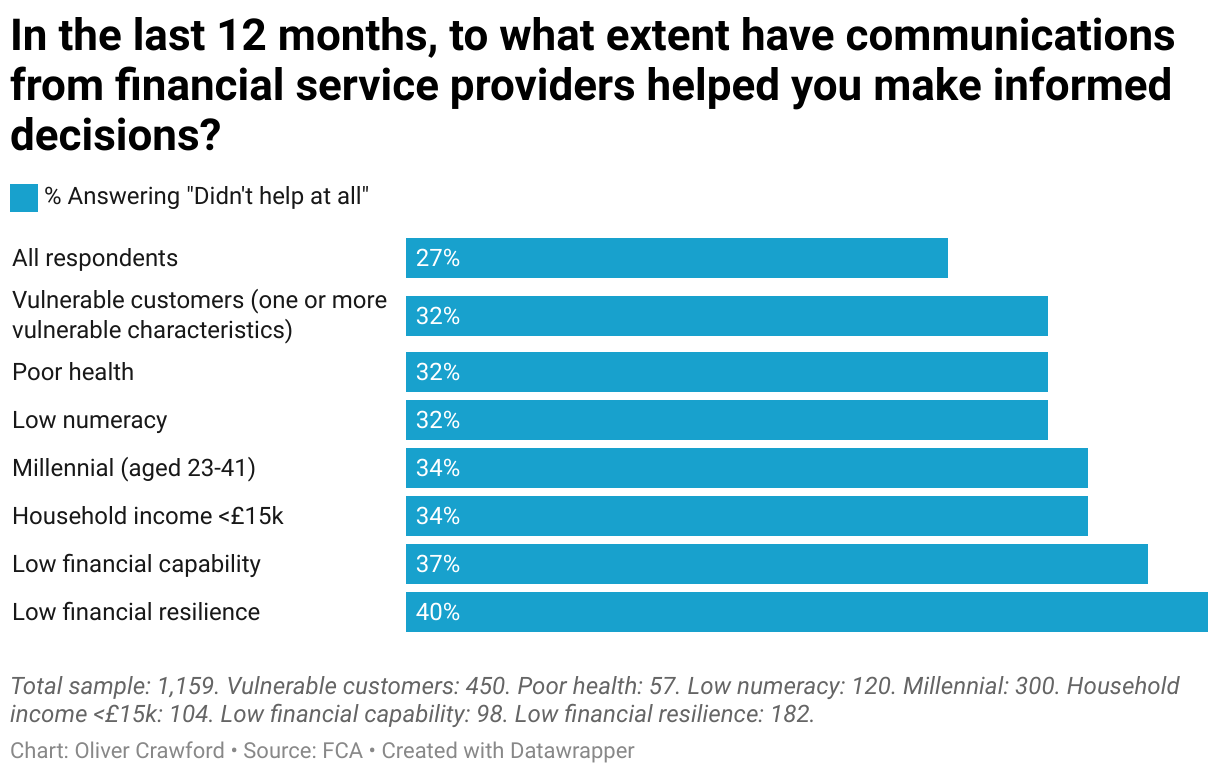

More concerning is the large minority of respondents who say that their providers' communications didn't help them at all in making informed decisions. Overall, 27% found the communications they received unhelpful, rising to 37% for those with low financial capability, and 40% for those with low financial resilience (a low ability to withstand financial shocks - roughly 30% of UK adults).

At Fairer Finance, we work with many companies to help them improve their communications. We have set out our principles on what makes for clear and simple communications in a guide we produced in partnership with the Association of British Insurers.

A huge amount of work has been done across the insurance industry to improve communications in the run up to the Consumer Duty, which came into force in July 2023. The Financial Lives survey data shows the scale of the task - hopefully the next survey will show some positive change as a result of the changes made to meet the challenge of the Consumer Duty.

To find out how Fairer Finance can help improve your communications or help you meet the challenge of the Consumer Duty more broadly, contact corporate@fairerfinance.com.

About the author